Last updated: 6/16/2016

Form 8928 Return Of Certain Excise Taxes Under Chapter 43 {8928}

Start Your Free Trial $ 13.99What you get:

- Instant access to fillable Microsoft Word or PDF forms.

- Minimize the risk of using outdated forms and eliminate rejected fillings.

- Largest forms database in the USA with more than 80,000 federal, state and agency forms.

- Download, edit, auto-fill multiple forms at once in MS Word using our Forms Workflow Ribbon

- Trusted by 1,000s of Attorneys and Legal Professionals

Description

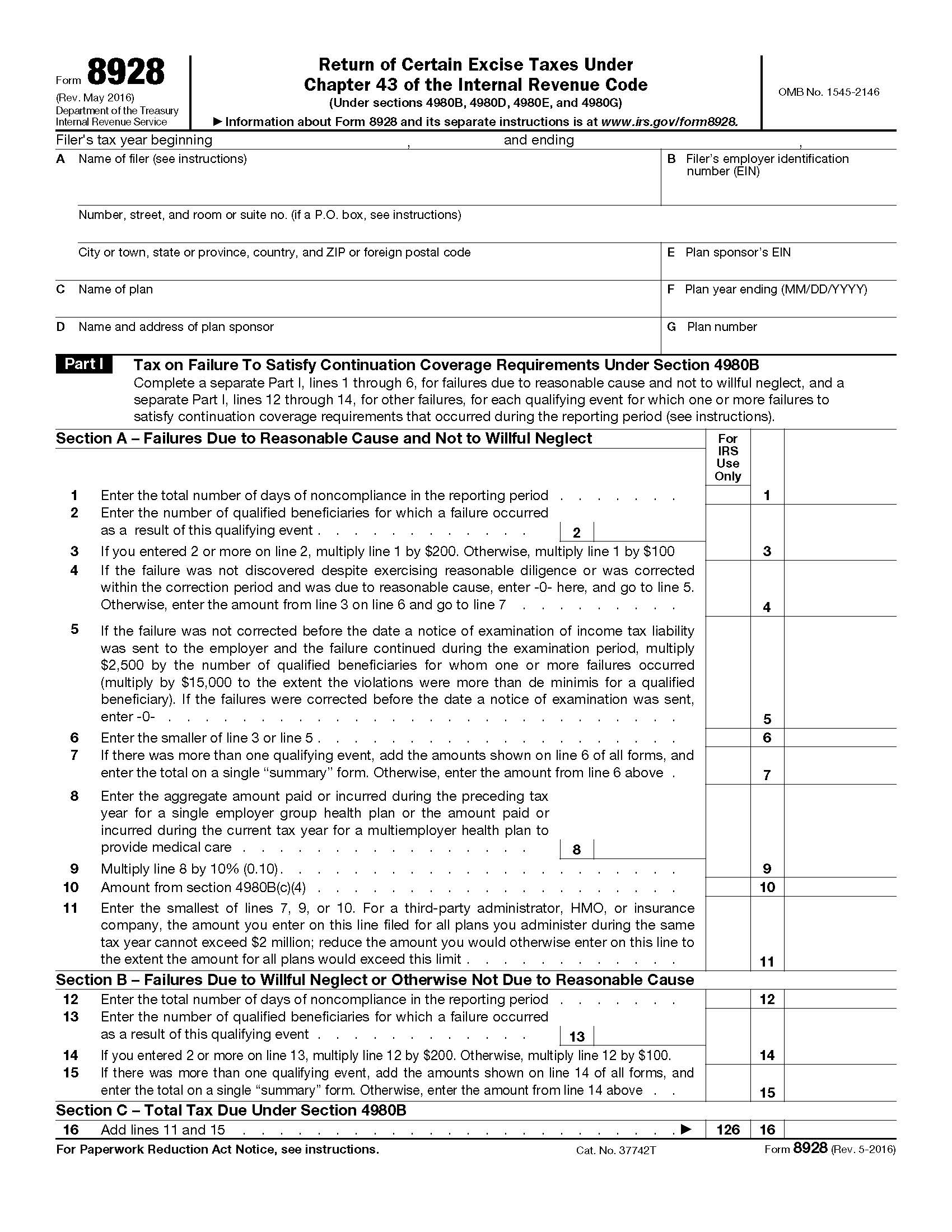

Form 8928 (Rev. May 2016), Return of Certain Excise Taxes Under Chapter 43 of the Internal Revenue Code (Under sections 4980B, 4980D, 4980E, and 4980G), Group health plans or employers file this form to report the tax due on the following failures. • A failure to provide a level of coverage of the costs of pediatric vaccines (as defined in section 2612 of the Public Health Services Act) that is not below the coverage provided as of May 1, 1993. • A failure to satisfy continuation coverage requirements under section 4980B. • A failure to meet portability, access, renewability, and market reform requirements under sections 9801, 9802, 9803, 9811, 9812, 9813, and 9815. • A failure to make comparable Archer MSA contributions under section 4980E. • A failure to make comparable health savings account (HSA) contributions under section 4980G. www.FormsWorkflow.com

Related forms

-

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/ -

Official Federal Forms/Department Of Treasury/